Client-side monitoring for fintech is the continuous observation and analysis of JavaScript execution, third-party script behaviour, and browser-layer data access within financial web applications. It covers what happens in the user's browser after the page loads: which scripts run, which form fields they touch, what data leaves the session, and whether any script behaviour changes between deployments. For fintech platforms, this is not a general hygiene practice. The combination of live payment data, regulated personal financial information, and strict compliance obligations makes the browser layer a high-value target and a heavily audited surface.

The fintech threat profile is specific. PCI DSS v4.0.1 requirements 6.4.3 and 11.6.1, mandatory since 31 March 2025, require financial platforms to authorise and inventory every script on payment pages and detect unauthorised changes to HTTP headers. GDPR Article 83(5) exposes platforms to fines up to EUR 20 million or 4% of global annual turnover when third-party scripts process personal data without a lawful basis. And the cost consequences are real: the IBM Cost of a Data Breach Report 2024 puts the global average data breach cost at USD 4.88 million, with financial services consistently among the highest-cost sectors. Supply-chain risk compounds this exposure. The June 2024 Polyfill.js compromise served malicious JavaScript to visitors of more than 490,000 websites through a single compromised CDN domain. Each of those sites had explicitly authorised the script origin, meaning standard CSP and hash monitoring would not have caught it. Fintech platforms that rely on third-party scripts for payment flows, KYC integrations, and analytics face this supply-chain vector directly. General client-side security tools are not designed around these requirements. Fintech security teams need platforms built for them. For the broader picture across both verticals, see our guide to client-side security for ecommerce and fintech platforms.

What is client-side monitoring for fintech? Client-side monitoring for fintech is the real-time inspection of browser-layer JavaScript activity on financial web applications, covering third-party script behaviour, form field access, data exfiltration signals, and compliance with PCI DSS and GDPR controls. It gives fintech security and compliance teams continuous visibility into what runs in the user's browser, what data those scripts can reach, and whether any unauthorised behaviour has occurred during a live session.

What Fintech Client-Side Monitoring Requires

Quick answer: Fintech platforms need client-side monitoring that covers PCI DSS 6.4.3 script authorisation and 11.6.1 header integrity monitoring, GDPR-signal visibility at the script level, complete session coverage without sampling gaps, QSA-validated audit evidence, and deobfuscated payload archival for incident response. Generic monitoring tools meet some of these requirements but rarely all of them.

PCI DSS 6.4.3 and 11.6.1 Compliance Readiness

Requirements 6.4.3 and 11.6.1 are not optional for any entity storing, processing, or transmitting cardholder data. Requirement 6.4.3 mandates a full inventory of payment-page scripts with authorisation records for each. Requirement 11.6.1 requires a mechanism to detect unauthorised changes to HTTP response headers and the contents of payment pages. A monitoring platform needs to produce evidence that satisfies a QSA, not just internal dashboards.

GDPR Script-Level Visibility

Under GDPR, the question is not only whether a cookie banner is present. The question is whether every script that executes on a user session has a documented lawful basis for any personal data it accesses. A platform that shows script names but not which form fields each script touches cannot answer that question. Fintech platforms operating in the EU need field-level visibility, not just domain-level script lists.

Full Session Coverage, No Sampling

Sampling is a standard performance compromise in general analytics tools, but it is operationally incompatible with compliance monitoring. A Magecart injection or data exfiltration event can affect a specific session type, a specific browser, or a specific checkout flow. A platform that monitors 10% or 20% of sessions has structural blind spots. Fintech deployments need 100% session coverage.

Deobfuscated Payload Archival

When a skimmer or supply-chain compromise is discovered, the incident response process requires forensic evidence: what the malicious script was doing, what data it accessed, and when the behaviour changed. Platforms that only alert on anomalies without preserving deobfuscated payload content leave security teams without the evidence needed for regulatory reporting or legal proceedings.

QSA-Validated Audit Evidence

The output of a monitoring platform must translate directly into QSA-acceptable documentation. Dashboards that require manual interpretation, exports that lack the required fields, or evidence packages that a QSA has never reviewed create friction and audit risk. Fintech teams need platforms where the compliance evidence is pre-validated by a recognised assessor.

The Platforms

1. cside

Best for: Fintech and regulated financial platforms that need QSA-validated PCI DSS compliance evidence, full session coverage, and GDPR form-field visibility.

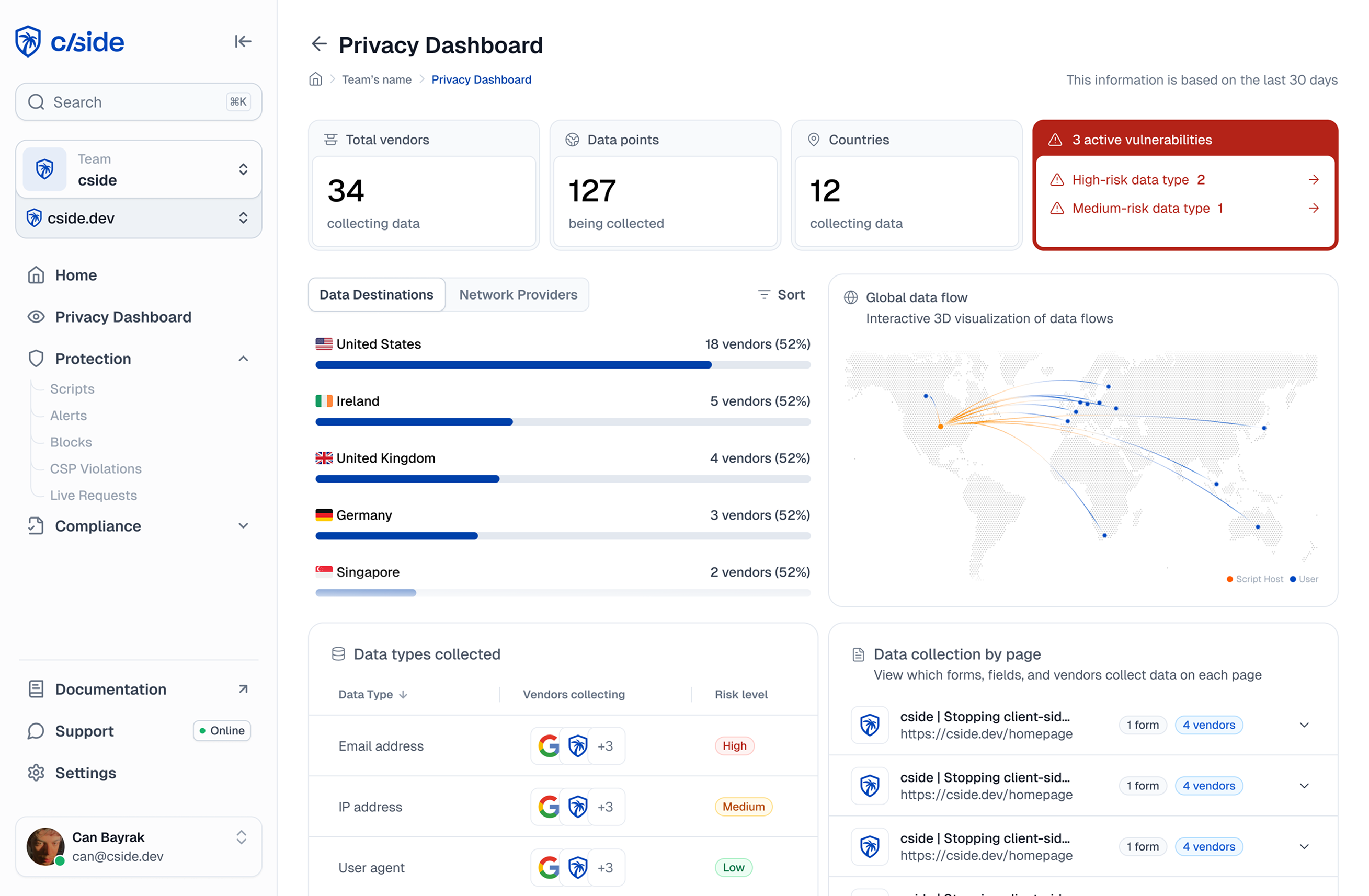

cside is a browser-layer script monitoring and client-side security platform built specifically for high-compliance environments. Its PCI Shield dashboard is QSA-validated by VikingCloud, producing audit-ready documentation for PCI DSS requirements 6.4.3 and 11.6.1 without requiring manual interpretation or spreadsheet exports. The platform covers 100% of real user sessions, which means no sampling gaps and no blind spots in live production traffic.

For GDPR compliance, cside provides session-level visibility into which scripts access which form fields. That field-touch mapping is the signal compliance teams need to demonstrate that third-party scripts are operating within their documented lawful basis. cside detected more than 300,000 previously unseen client-side attack signals in Q1 2025 (cside product data), which reflects the breadth of the threat surface the platform monitors across the customer base.

Deobfuscated payload archival means that when an incident occurs, the forensic record is already there. Self-service onboarding and transparent pricing make it practical for fintech security teams who need fast deployment without a long procurement cycle. For fintech teams who want more detail on the PCI DSS compliance use case or GDPR script visibility, both pages walk through the specific controls.

2. Reflectiz

Best for: Enterprises with complex third-party ecosystems that prioritise website risk scoring and risk posture reporting.

Reflectiz monitors third-party scripts through a sandboxed browser environment that simulates page execution rather than instrumenting live sessions. This gives visibility into script behaviour without deploying code to production, which some security teams prefer for reducing operational dependencies. The tradeoff is that sandboxed execution does not always replicate real-user session behaviour, particularly for scripts that activate conditionally based on user actions.

Reflectiz offers PCI DSS monitoring capabilities and GDPR-related vendor risk reporting. The platform positions itself as a risk governance tool, with reporting workflows oriented towards compliance documentation and third-party vendor management. Evidence packages for QSA reviews are available but their validation status varies by assessor.

The platform is enterprise-focused with corresponding pricing and implementation timelines. Fintech teams with established procurement processes and a priority on portfolio-level vendor risk visibility may find it a reasonable fit, though the sampling model and sandbox execution approach differ meaningfully from session-instrumentation platforms.

3. Source Defense

Best for: Organisations looking for script sandboxing controls with a focus on blocking unauthorised script behaviour in real time.

Source Defense takes an active control approach, using client-side sandboxing to limit what third-party scripts can do in the browser even before a threat is detected. This is a different posture than pure monitoring: the platform attempts to prevent data access by untrusted scripts at the policy level, rather than just alerting on it after the fact. That prevention-first model appeals to compliance teams who want enforcement rather than observation.

PCI DSS coverage is present in the product, with controls that map to requirements 6.4.3 and 11.6.1. GDPR-related enforcement is built around the sandboxing model, restricting script access to personal data based on policy rules. The platform does require more configuration time to build and maintain effective sandbox policies for complex fintech environments.

Session coverage is limited by the sandboxing architecture: the platform monitors what it enforces, but deep forensic visibility into non-sandboxed script behaviour is more limited. Fintech teams prioritising active prevention over forensic depth may find Source Defense's model well-matched to their risk posture.

4. Jscrambler

Best for: Development teams that want to combine client-side code protection with browser monitoring in a single platform.

Jscrambler's original product is JavaScript obfuscation and code protection, and its monitoring capabilities have grown from that foundation. The platform offers webpage integrity monitoring that covers PCI DSS 6.4.3 and 11.6.1 requirements, and it integrates with development workflows in a way that reflects its origin in the developer toolchain. Teams that already use Jscrambler for code protection will find the monitoring layer a natural extension.

GDPR-related script visibility is present but oriented more towards script inventory than field-level session behaviour. Fintech teams that need granular visibility into which scripts access which form fields during live user sessions may find the level of detail less specific than platforms purpose-built for that compliance requirement. The product is more powerful when code protection and monitoring are both in scope.

Pricing and packaging are enterprise-focused. The platform makes most sense for fintech engineering and security teams that want to consolidate code protection and monitoring, rather than pure compliance teams evaluating monitoring tools in isolation.

5. HUMAN Security Page Protect

Best for: Fintech platforms with existing HUMAN Security relationships that want to extend bot protection into client-side integrity monitoring.

HUMAN Security's Page Protect extends the company's bot detection capabilities into the browser layer, adding script monitoring and payment-page integrity controls. For fintech teams already using HUMAN's bot management product, Page Protect is a logical adjacency because it shares the same platform relationship and commercial arrangement. PCI DSS 6.4.3 and 11.6.1 coverage is included.

The product's design centre is integrity protection rather than compliance documentation depth. Fintech teams that need rich audit-ready evidence packages with QSA validation will need to confirm how the platform's output maps to their specific assessor's requirements. GDPR script-level visibility is available but is not the primary design centre of the platform.

Session coverage follows the platform's detection model. Fintech teams that are evaluating Page Protect specifically for compliance purposes, rather than as an extension of an existing HUMAN relationship, should assess whether the compliance evidence workflow meets their QSA's documentation standards before committing.

6. Feroot

Best for: Privacy-focused fintech and healthtech teams that need GDPR and CCPA data flow mapping alongside PCI DSS controls.

Feroot positions itself explicitly around data privacy and regulatory compliance, with strong GDPR and CCPA data flow visibility as its design centre. The platform maps data flows from third-party scripts with a focus on privacy regulation compliance, which makes it a natural fit for fintech teams where GDPR is as important as PCI DSS. The privacy-first framing means the compliance documentation tends to be detailed and regulator-friendly.

PCI DSS support covers requirements 6.4.3 and 11.6.1. The platform's strength is in the intersection of privacy regulation and script monitoring, so fintech teams operating in multiple regulated jurisdictions may find the breadth of its compliance mapping useful. Forensic depth and payload archival are more limited compared to platforms designed primarily for security incident response.

Feroot is a reasonable choice for compliance-led fintech teams where the primary driver is demonstrating regulatory data flow control, and where the security incident response use case is a secondary priority.

Platform Comparison

| Platform | Data residency / self-hosting | GDPR script visibility | PCI DSS 6.4.3 + 11.6.1 | Full session coverage | QSA-validated evidence |

|---|---|---|---|---|---|

| cside | Self-hosted option | Yes (field-level) | Yes | Yes (100%, no sampling) | QSA-validated (VikingCloud) |

| Reflectiz | Limited | Partial | Yes | Via sandboxing | Partial |

| Source Defense | Limited | Partial | Yes | Via sandboxing | Partial |

| Jscrambler | Limited | Partial | Yes | Partial | Partial |

| HUMAN Security Page Protect | Limited | Partial | Yes | Partial | Partial |

| Feroot | Limited | Yes (data flow) | Yes | Partial | Partial |

How to Choose for Fintech

Quick answer: Start with your most urgent compliance driver. If PCI DSS 4.0.1 audit readiness is the priority, require QSA-validated evidence and 100% session coverage. If GDPR field-level script control is the priority, require form-field-touch visibility. If both apply, require both, because most platforms satisfy one better than the other.

If your primary concern is PCI DSS 4.0.1 audit readiness: Choose a platform with QSA-validated evidence workflows, not just dashboards that map to PCI controls. The difference matters in a live QSA review. cside's VikingCloud-validated PCI Shield is the only option in this list with independent assessor validation built into the product.

If your primary concern is GDPR-compliant third-party script governance: Choose a platform that reports which scripts access which form fields, not just which scripts load. Domain-level script inventories are insufficient for demonstrating lawful basis. cside and Feroot both offer deeper visibility here, though with different design centres.

If your primary concern is incident response and forensic evidence: Choose a platform that retains deobfuscated payload content and session-level behavioural records. An alert without a preserved payload leaves the incident response team reconstructing events from incomplete signals.

If your primary concern is active prevention rather than monitoring: Source Defense's sandboxing approach is the most prevention-oriented option in this list. The tradeoff is less forensic depth. Most fintech security teams need both, which argues for a platform that monitors first and has blocking capability as a secondary control.

Evaluation Checklist for Fintech Security Teams

Quick answer: Before committing to a fintech client-side monitoring platform, verify five things in a proof-of-concept: QSA-accepted evidence format, 100% session coverage (not sampled), form-field-touch visibility for GDPR, deobfuscated payload retention, and GDPR data flow export capability. A platform that passes all five is genuinely ready for a fintech compliance audit.

Before committing to a platform, verify these five capabilities in a proof-of-concept or demo:

- QSA evidence validation. Ask the vendor whether their PCI DSS compliance evidence has been reviewed and accepted by a named QSA assessor. Dashboards that map to PCI controls are not the same as pre-validated evidence packages.

- Session sampling policy. Confirm whether the platform monitors 100% of sessions or operates on a sample. Request documentation of the session coverage methodology.

- Form-field-touch visibility. Ask the vendor to demonstrate which form fields each third-party script reads during a live session, not just which scripts are present.

- Deobfuscated payload retention. Ask whether the platform retains readable script payloads for incidents and for how long. Alert metadata alone is insufficient for regulatory notification.

- GDPR data flow mapping. Ask whether the platform can generate a GDPR-compliant record of which scripts accessed which data fields, and whether that record is exportable for regulatory submissions.