In This Blog:

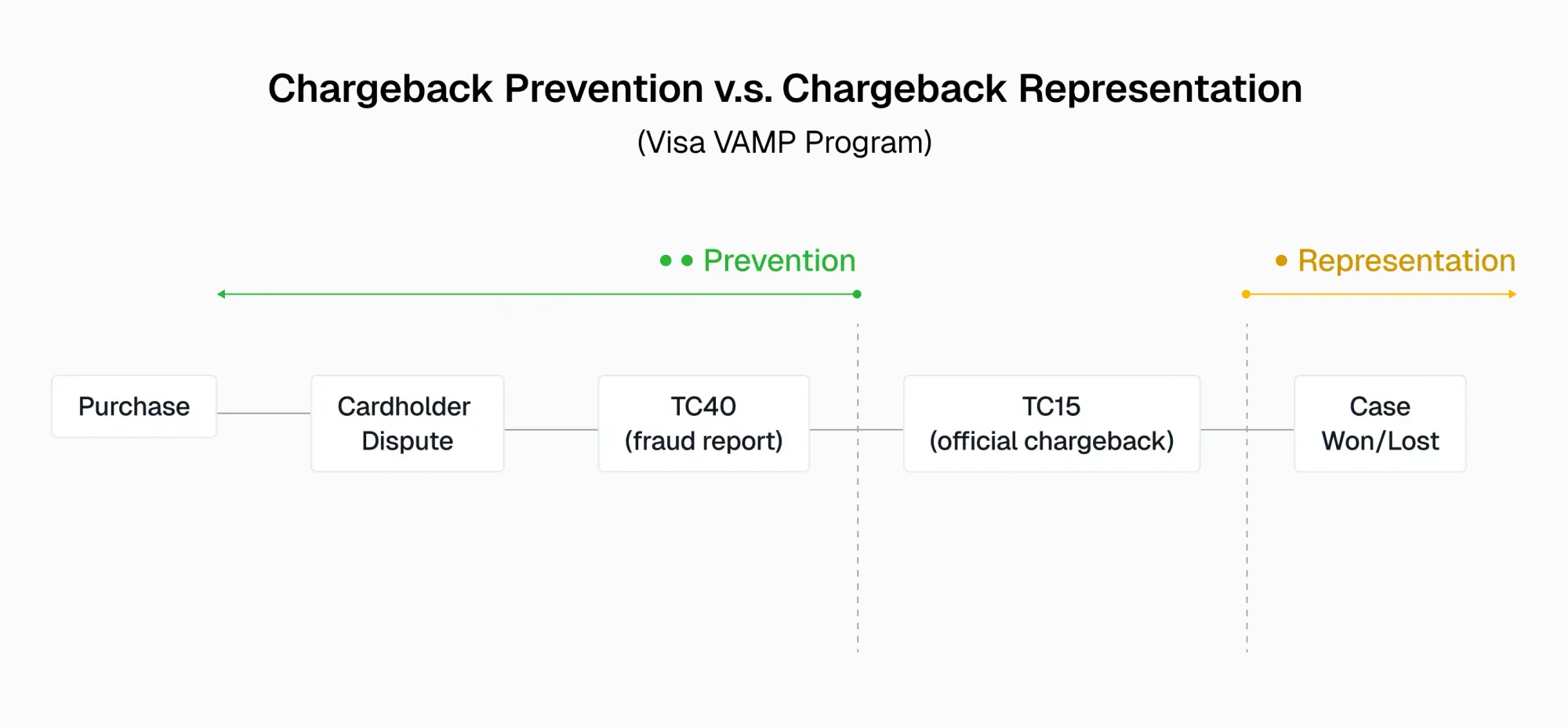

- Chargeback prevention v.s. chargeback representation

- Underutilized chargeback prevention tools

- Top chargeback prevention vendors

- Understanding chargeback prevention programs (RDR, CDRN, CE 3.0)

Visa’s new VAMP thresholds have redrawn the line between “safe” and “at risk.” Previously clean merchants are now in a danger zone. And we’ve seen a surprising amount of merchants rely on a chargeback defense approach that was designed for 2018 fraud patterns. Those stacks haven’t caught up to the change in consumer behavior that is driving up first party misuse. First-party fraud costs merchants upwards of $50 Billion a year (according to Mastercard). A category that used to be primarily “accidental” has blown up due to refund schemes and cyber shoplifting.

With tightened VAMP thresholds (that counts fraud and chargebacks in oneratio), fraud teams going into 2026 need a way to:

- Reduce TC15s (chargebacks) and TC40s (fraud reports) for VAMP programs

- Avoid refunds (lost revenue)

- Cut down chargeback fees ($15 to $100+ on avg.)

- Remain in good standing with acquirers - or on the flip side - acquirers need to keep their portfolio of merchants clean.

That’s where chargeback prevention comes in. Some programs help merchants reduce TC15s while other programs can eliminate TC15s, TC40s, and refunds altogether on eligible cases.

Why Chargeback Prevention is Important in 2026

Prevention should be the top priority for Risk & Fraud teams going into 2026. Chargeback representation is still a crucial part of a chargeback defense strategy, but “won” cases still count towards VAMP ratios.

| Aspect | Recovery | Prevention |

|---|---|---|

| When it happens | After the chargeback is filed | Before a chargeback becomes official |

| Goal | “Win” the chargeback, recover revenue from refund | Block the chargeback. Prevents TC15s. Can prevent TC40s. Can prevent refunds. |

| Tools | Software/services that fight chargeback cases | Visa: RDR, CDRN, CE 3.0 + device fingerprinting |

| Cost | High when internally done (manual reviews, fees, penalties). Performance-based with vendors. | Low (automation, data capture) |

| Impact on VAMP ratio | Still counted | Depends on program - TC15s or TC40s not counted |

| Risk mindset | Reactive | Proactive |

Consumer Behavior is Driving First-Party Misuse

Merchants are fighting against the current from both sides. Both Visa and Mastercard have strict rules, while rates of first-party misuse from consumers are skyrocketing. The biggest fraud threat going into 2026 isn’t a hacker in a dark room, but rather consumers themselves. Some of these cases are unintentional, like family fraud. But many are consumers deliberately exploiting refund systems or filing false disputes because they know merchants would rather issue a quick refund than risk a chargeback on their record. Traditional fraud tools were never designed to stop a wave of cyber shoplifting.

Underutilized Tools for Chargeback Prevention

Most merchants with transaction volumes that qualify for VAMP already use the major chargeback prevention programs (CE 3.0, RDR, CDRN, and Order Insight). But few are being proactive in preparing for the VAMP squeeze that will take place in 2026.

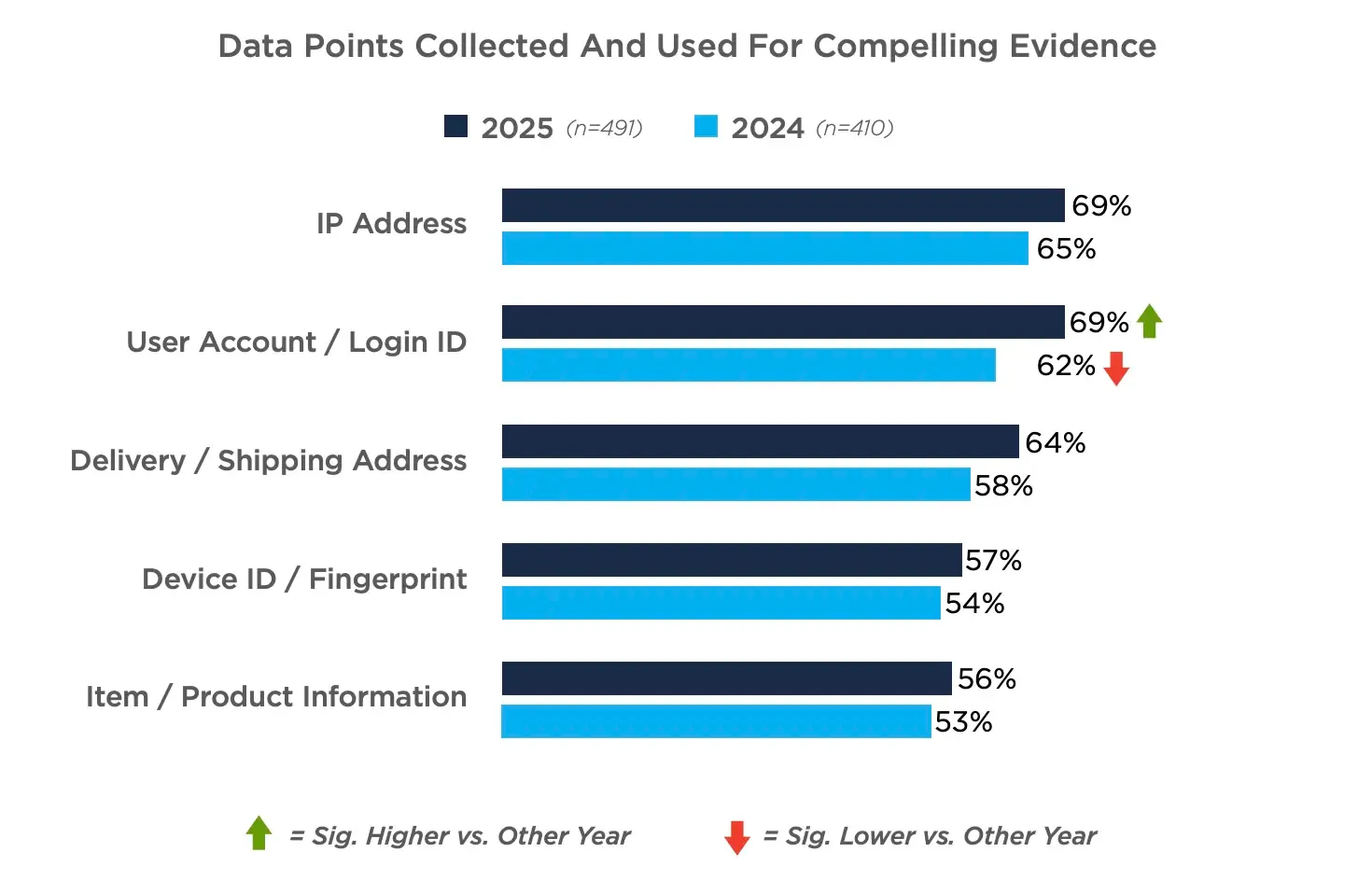

1. Device Fingerprinting = More Compelling Evidence Wins

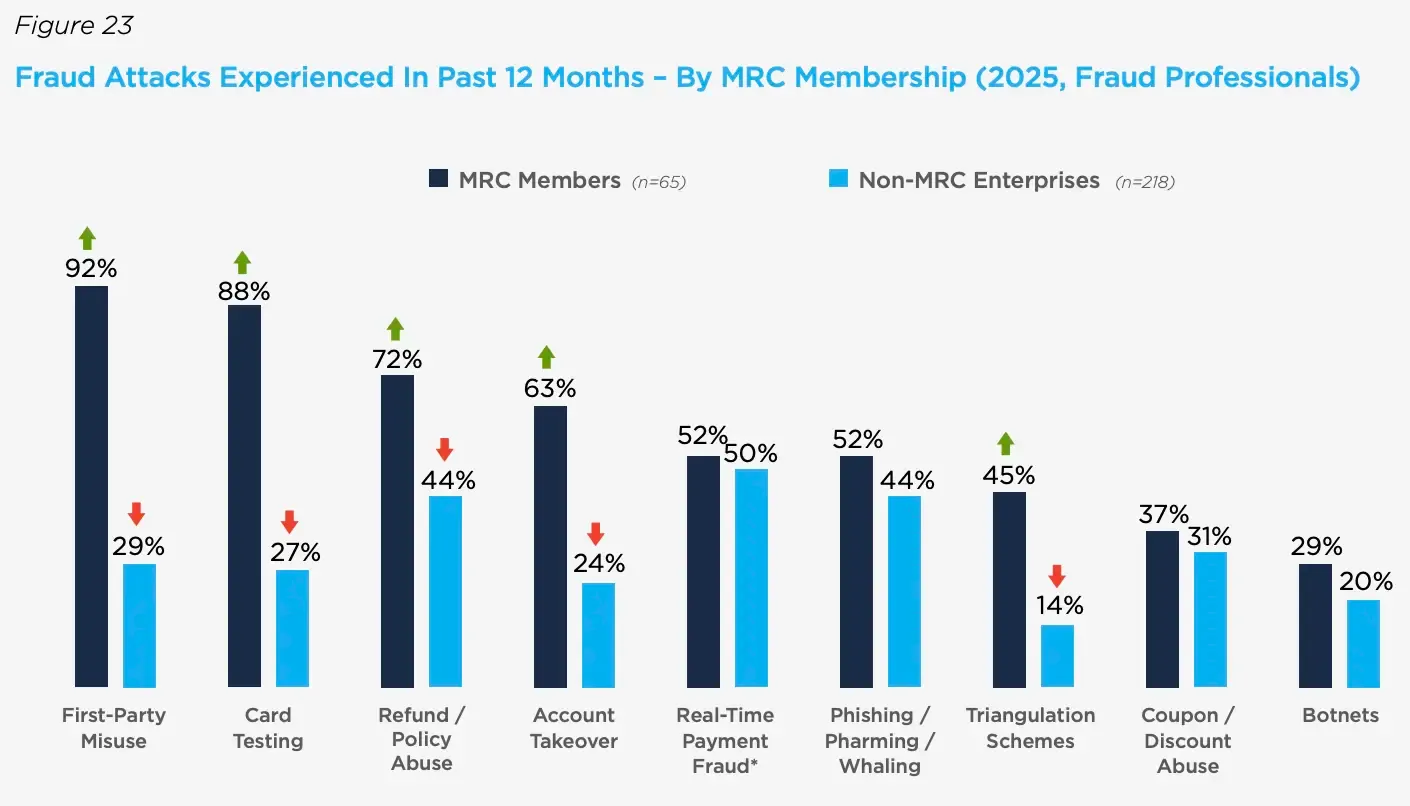

Source:Merchant Risk Council

According to merchants surveyed in the Merchant Risk Council 2025 Global Fraud and Payments Report, 87% of merchants are using the Compelling Evidence program to fight first party misuse, but only 57% of merchants are using Device Fingerprints. That means nearly half of merchants are missing the strongest data signal Visa accepts to prove a trusted device match.

Integrating device fingerprinting is far simpler than most merchants realize and can be plugged in directly into your chargeback stack. This data quality gap often comes from vendors advertising “device ID” collection while relying mainly on IP addresses and cookies, which provide only a partial view of the device behind the transaction. A dedicated device fingerprinting solution is less invasive than cookies and uses privacy compliant signals to create a unique hash for each device.

2. AI Bot Detection & Card Testing Bot Defense

Source:Merchant Risk Council

Card testing bots are another massive problem. 88% of merchants in the MRC (companies like AirBnB and Blizzard Entertainment) experienced this fraud type in 2025. While card testing doesn’t always lead directly to chargebacks, it inflates authorization costs and contributes to Visa’s VAMP Enumeration Ratio, a metric Fraud teams must also monitor closely.

At the same time, AI-driven bots are creating a new class of threats. Stealing customer data, pirating digital content, and probing checkout flows for vulnerabilities.

Both of these fraud vectors are addressed with a client-side security solution. The “client-side” here refers to the browser environment (where real users and bad bots interact with your website). Bad bots leave telltale clues on the client-side that are missed by traditional fraud tools as they tend to only look at network-level data. Client-side monitoring tools catch this behavior earlier and offer governance settings to give fraud teams more control.

Top Chargeback Prevention Vendors (2026)

Chargeback Prevention Vendor Comparison Matrix:

| Vendor | CE 3.0 Ready | Device Intelligence | Post-Transaction Prevention | Pre-Transaction Prevention | Vendor Focus |

|---|---|---|---|---|---|

| Chargebacks911 | Yes | Strong (partnership with cside) | Alerts, Rapid Resolution, CE 3.0 + additional tools |

Prevention products are focused on Post-Transaction | Specialized in chargeback management & representation |

| Kount | Yes | Limited | Alerts, Rapid Resolution, CE 3.0 + additional tools |

Omniscore, Identity Verification | Trust & Safety / fraud prevention suite |

| Riskified | Yes | Limited | Alerts, Rapid Resolution, CE 3.0 + additional tools |

Fraud Decisioning, Policy Protect | eCommerce fraud prevention platform |

1. Chargebacks911

Founded in 2011 by merchants who had experienced first-hand the pain of chargebacks eating into profits. Built with a merchant-centric approach since conception this company has risen to be a trusted end-to-end dispute management partner. As the name suggests this vendor is deeply specialized in the chargeback space, offering prevention and representation solutions.

Features: Post-Transaction Chargeback Prevention

- **Compelling Evidence 3.0:**Introduced by Visa in 2023, Compelling Evidence 3.0 allows merchants to block first-party fraud disputes (card-not-present cases) by proving a link between the disputed transaction and previous legitimate purchases made from the same device and customer.

- **Order validation (Visa Order Insight and Mastercard Consumer Clarity):**Instantly provides banks with merchant data to clarify billing details. This tool can resolve disputes before they escalate to formal chargebacks.

- **Visa Rapid Dispute Resolution (RDR):**Resolves eligible disputes before they become chargebacks by auto-refunding transactions based on rules set by the merchant.

- **Chargeback Alerts:**Visa CDRN and Mastercard Ethoca alert merchants on disputes directly from issuing banks. Merchants/chargeback management teams can resolve the issue (through a refund or direct communication with the customer) before it escalates into a formal chargeback.

Pros

- Purpose-built for chargeback management and post-transaction chargeback prevention. Great fit for merchants seeking a dedicated dispute solution without paying for bundled fraud tools they don’t need.

Reviews

Review taken from G2 Reviews →

“Chargebacks911's best practices have changed the way we manage chargebacks and taken us from a constant state of panic to being coherent and data driven in our approach… we are able to effectively leverage tools that protect our business and our customers.” - Jessica G. (5/5)

Pricing

Pricing is variable per customer based on transaction volume and potential revenue savings. There is an interactive ROI calculator on their website. A custom quote is required for an accurate price estimate.

2. Kount

Positioned as a “Trust and Safety” solution, Kount offers anti-fraud tools that extend into identity verification and compliance as well as payment fraud. Owned by Equifax, Kount taps into a global data network that helps merchants spot high risk behavior. With a diverse suite of solutions Kount remains a long-standing player in the world of chargeback management.

Features: Post-Transaction Chargeback Prevention

- Order validation(Visa Order Insight and Mastercard Consumer Clarity)

- Rapid Dispute Resolution (RDR)

- Compelling Evidence 3.0

- Prevention Alerts

Features: Pre-Transaction Chargeback Prevention

- **Real-Time Risk Scoring (Omniscore):**AI and machine learning models generate a score for each transaction linked to fraud probability. Rules can be customized to accept/decline transactions.

- **Identity Verification:**Address verification service and 3D Secure 2.0 to send transaction details to the issuer for real-time verification.

- **Negative Lists:**Maintain a list of customers who have previously filed a chargeback or engaged in fraudulent activity. Orders from this list can be flagged or canceled.

Note: The features highlighted above are a summarized list from our research that we found relevant to this article. Each vendor has a much wider list of features in their product suite.

Pros

- Robust identity verification and pre-transaction fraud analysis capabilities.

Reviews

Review taken from G2 Reviews →

“We use Kount to create custom rules that we use to capture the relevant information from all sources. Kount applies the AI expertise to analyze massive interactions and offer safety rating for easy management.” - Kovai L. (4.5/5)

Pricing

Pricing for Kount is not publicly listed. A custom quote is required based on the mix of fraud prevention and chargeback management features you need

3. Riskified

Riskified is a fraud prevention solution focused on ecommerce merchants. With ecommerce specific capabilities like adaptive checkout, Riskified is another well established vendor with several products for chargeback prevention and revenue protection.

Features: Post-Transaction Chargeback Prevention

- Compelling Evidence 3.0

- Rapid Dispute Resolution (RDR)

- Chargeback Alerts

Features: Pre-Transaction Chargeback Prevention

- Fraud Decisioning: Analyze incoming orders against an extended data network. Based on machine learning models, an “approve” or “decline” decision for each transaction is provided.

- **Policy Protect:**Data engine that shows merchants which customers are trustworthy and profitable. The “right” customers can be rewarded with promos.

Note: The features highlighted above are a summarized list from our research that we found relevant to this article. Each vendor has a much wider list of features in their product suite.

Pros

- Unique features for online commerce merchants including integration with loyalty programs.

Reviews

Review taken from G2 Reviews →

“Riskified is a really helpful tool to minimise risk on sales orders. It uses a lot of different triggers such as IP, Address, Bank Details to determine a potential outcome.” Katie B. (4/5)

Pricing

Pricing not listed publicly. Comments left by customers indicate a pay as you go pricing model based on volume and risk profile.

Understanding Chargeback Prevention Tools/Programs

Chargeback management vendors plug into the same core programs put in place by Visa and Mastercard. It’s easy to get lost in the sea of acronyms The jargon can get confusing, so let’s take a look at each:

What is Visa’s Rapid Dispute Resolution (RDR):

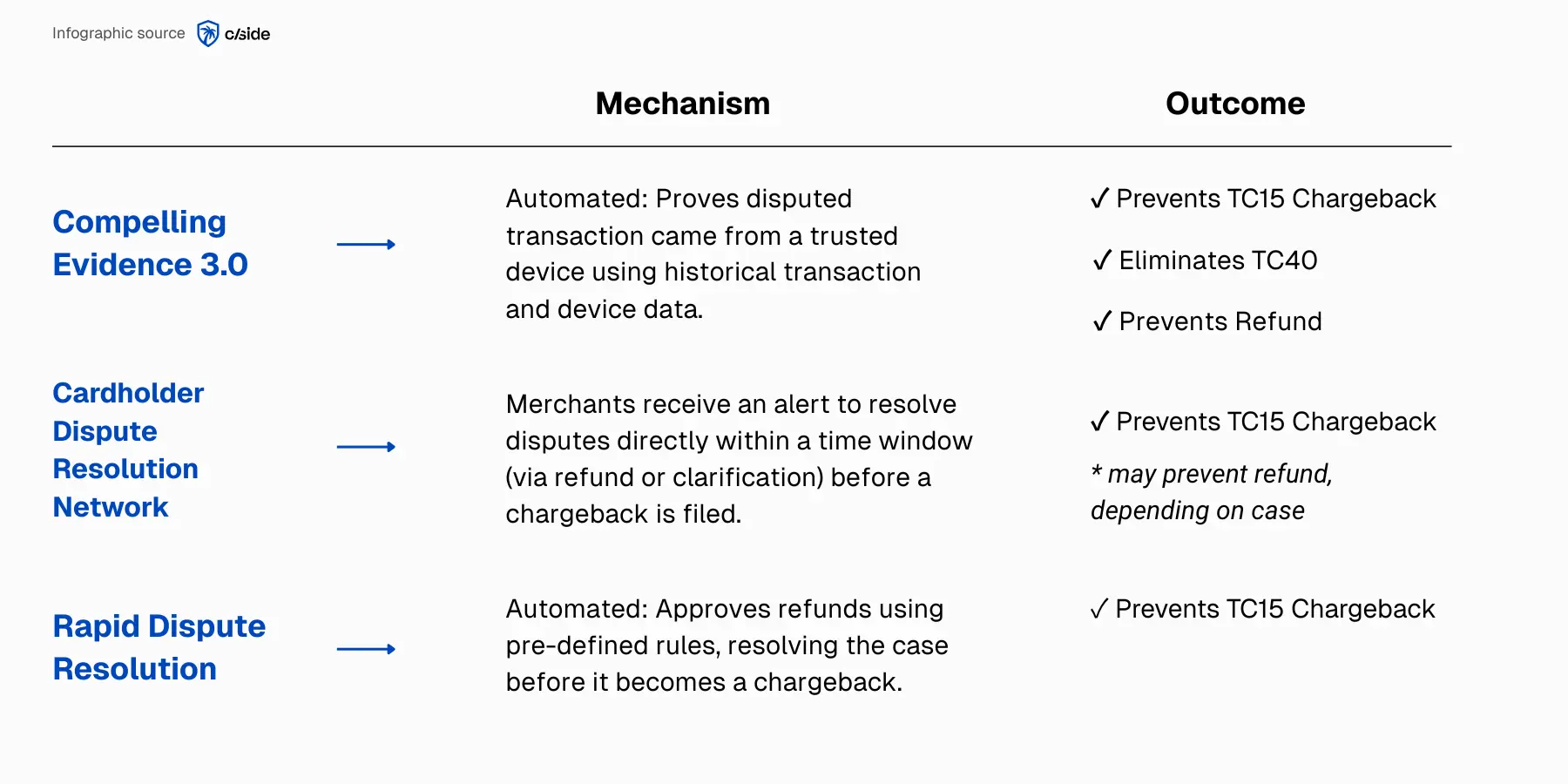

- Visa’s Rapid Dispute Resolution (RDR) is an automated system that allows merchants to instantly refund eligible transactions before they turn into chargebacks. RDR uses predefined merchant rules to determine whether to issue a refund, helping prevent formal disputes (TC15s) and keep VAMP ratios within safe limits.

- Merchant Scenario: A customer disputes a $20 subscription renewal. Instead of the case turning into a chargeback (where fees and ratio risk might cost more than the refund), RDR automatically triggers an instant refund according to the merchant’s refund rule, closing the dispute before it ever hits Visa’s chargeback system.

What is Visa’s CDRN?

- Visa’s Cardholder Dispute Resolution Network (CDRN) alerts merchants in real time when a customer disputes a charge, giving them a short window to respond to the issue directly. By responding quickly, often through a refund or clarification, merchants can prevent the case from escalating into a formal chargeback.

- Merchant Scenario: A customer doesn’t recognize a $75 online order and calls their bank. The bank issues a CDRN alert to the merchant, who verifies the order and issues a same-day refund stopping the dispute from becoming a chargeback.

What is Visa’s Compelling Evidence 3.0?

- Introduced by Visa in 2023, Compelling Evidence 3.0 (CE 3.0) allows merchants to deflect first-party fraud disputes by proving a clear link between the disputed transaction and prior legitimate purchases from the same device and account/customer. This program prevents disputes from ever becoming official chargebacks (TC15s), removes TC40s on won cases, and does not require the merchant to issue a refund.

- Merchant Scenario: A customer claims they didn’t authorize a $200 online purchase. Visa’s CE 3.0 system matches the transaction to the same device and account used for past successful purchases, ruling this as a first-party misuse situation and deflecting the dispute instantly.

What is Verifi (Visa)?:

Verifi, acquired by Visa in 2019, is an infrastructure that allows issuing banks to request merchant data directly. This integration lets merchants share transaction data or issue instant refunds to resolve cardholder disputes.

What is Ethoca (Mastercard)?:

Ethoca, owned by Mastercard, is a global collaboration network for merchants and banks to exchange fraud and dispute data in real time.

What is Order Insight (Visa)?:

Order Insight, part of the Verifi suite, lets merchants provide detailed transaction data, like product details or device info, directly to banks during a cardholder inquiry.

Verifi and Ethoca form the technology infrastructure that helps banks instantly access the data they need from merchants. When a cardholder disputes a transaction, the bank classifies it under a specific reason code and uses one of these programs to request the merchant’s transaction data in the proper format.

These programs work in harmony with chargeback management vendors. Vendors handle the heavy lifting of collecting, storing, and integrating merchant data to maximize the merchant win rate of these programs.

Post-transaction v.s. Pre-Transaction Chargeback Prevention

Not all chargeback prevention happens at the same stage of the customer journey. The key difference comes down to when fraud or dispute risk is detected. Before a transaction is approved (pre-transaction) or after it’s completed (post-transaction):

Pre-Transaction Chargeback Prevention

Centered on stopping fraudulent or high-risk transactions before payment authorization.

- How it works: Typically, a risk score is created by predictive models that look at behavioral analytics, device data, known lists of fraudulent customers, and extended data networks to determine the probability of a fraudulent transaction.

- The goal: Block fraudulent customers from making a purchase.

- Example: A fraud detection platform flags a login from a suspicious device and automatically declines the purchase before the order is processed.

Post-Transaction Chargeback Prevention

Happens after a transaction has gone through (payment authorized), but beforethe dispute becomes an official chargeback, and in some cases before a cardholder dispute is made.

- **How it works:**Programs like Compelling Evidence 3.0 or Rapid Dispute Resolution are used to resolve cardholder disputes before they become official chargebacks. Transaction, account, and device data is analyzed by Verifi to make a decision.

- The goal: Block fraudulent customers from filing a chargeback.

- **Example:**An ecommerce customer claims their card was stolen to make a purchase on a travel site, but the merchant provides device fingerprinting and CE 3.0 data to prove it was made from the same device and account as previous legitimate purchases, blocking the dispute before it becomes a chargeback.

Chargeback Prevention v.s. Chargeback Representation

While they sound similar, chargeback prevention and chargeback representation****solve very different problems.

Chargeback Prevention Tools

Prevention tools focus on stopping cardholder disputes from becoming chargebacks cases.

- **Result:**Reduced TC15s (chargebacks) counted towards VAMP ratio, and with some programs reduced TC40s (fraud reports) and no refund required.

- **Why this matters:**Merchants (or acquirers) that go above a VAMP threshold are placed in a high risk program with hefty additional fees ($6-$8 per chargeback) and possible restrictions.

Chargeback Representation Solutions

Also associated with “Chargeback Insurance” or “Chargeback Guarantees”, these solutions focus on winningchargeback cases after they have been filed.

- **Result:**Recovered revenue from the refund.

- **Why this matters:**Some industries will inevitably face high rates of chargebacks. For these, there is a straightforward ROI to have a team fighting cases and winning back revenue.