In This Blog:

- Why device fingerprinting is the strongest signal for CE 3.0

- How client-side intelligence reduces TC40s and Chargebacks

- How to add client-side intelligence to your chargeback stack

You ship the order, the customer gets it, and then calls the bank to say: “I didn’t make that purchase”. That’s friendly fraud, and it’s been skyrocketing. Visa is about to make VAMP ratios even tighter, but they’ve also given merchants a new line of defense: Compelling Evidence 3.0, a way to block disputes before they become official charge backs.

“The old way was fighting chargebacks after the damage. The new way is to block them upstream with a prevention strategy. This helps merchants cut down charge back fees altogether, Keep VAMP ratios within thresholds to avoid penalties, and deflect cardholder disputes in seconds instead of wasting weeks fighting cases.”

— Mike Kutlu, Client-side Security Consultant, cside

According to the Merchant Risk Council’s 2025 global payment fraud report, 87% of surveyed merchants are submitting compelling evidence to fight off first-party misuse, but only 57% are collecting device fingerprinting/device ID level data to support their compelling evidence strategy.

Changes to VISA’s VAMP Ratios

By 2026, Visa is dropping dispute ratios to

- 0.9% for merchants

- 0.5% for acquirers (banks, financial institutions).

Back in 2024, these ratios were 2.2% for merchants and 1.5% for acquirers. They’ve been cut by more than half and expected to tighten further. Since VAMP ratios include both TC40s (reports of fraudulent transactions) and TC15’s (all chargebacks, fraud or non-fraud related), companies that were previously in a safe threshold are now feeling the pressure for protection.

If you breach your VAMP ratio, it's 6-8 dollars per TC15, if you're over 0.7% it will be even higher and VISA keeps changing the fees.

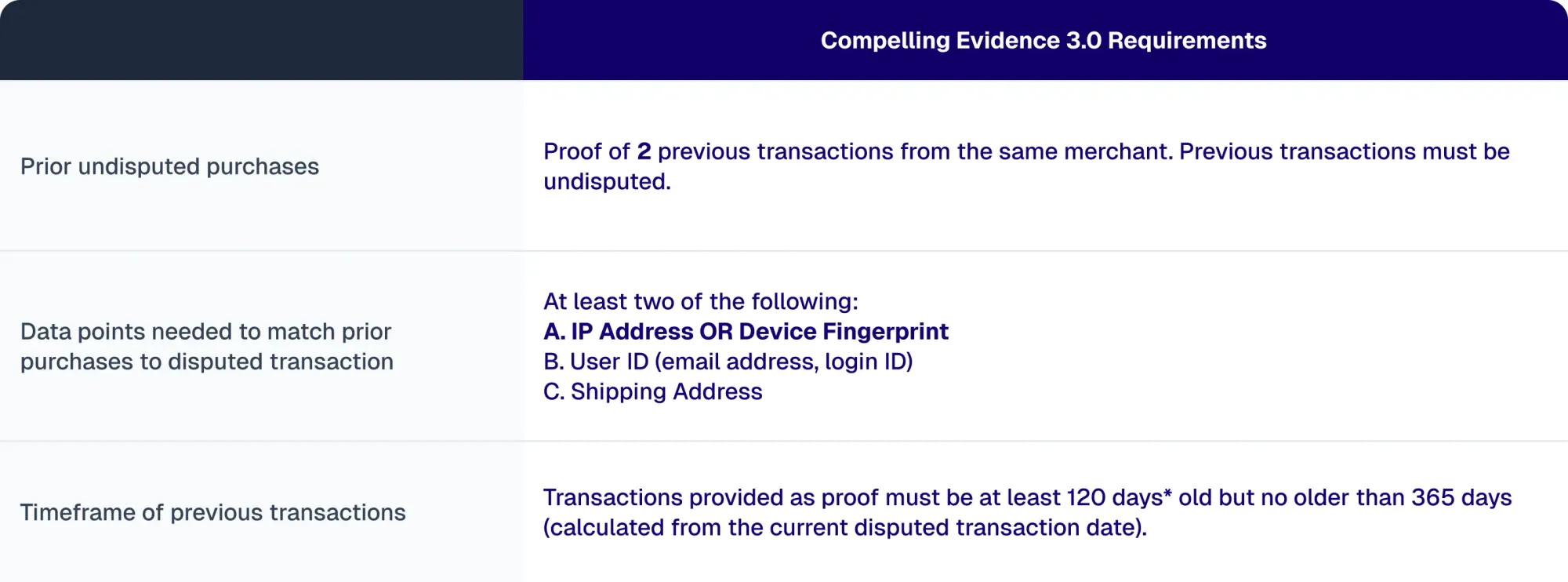

VISA Compelling Evidence 3.0 Requirements:

To see where device fingerprinting makes a difference, let’s start with what Visa’s CE 3.0 really asks for.

Table: Compelling Evidence 3.0 Requirements

Why Device Fingerprinting is The Strongest Signal for CE 3.0

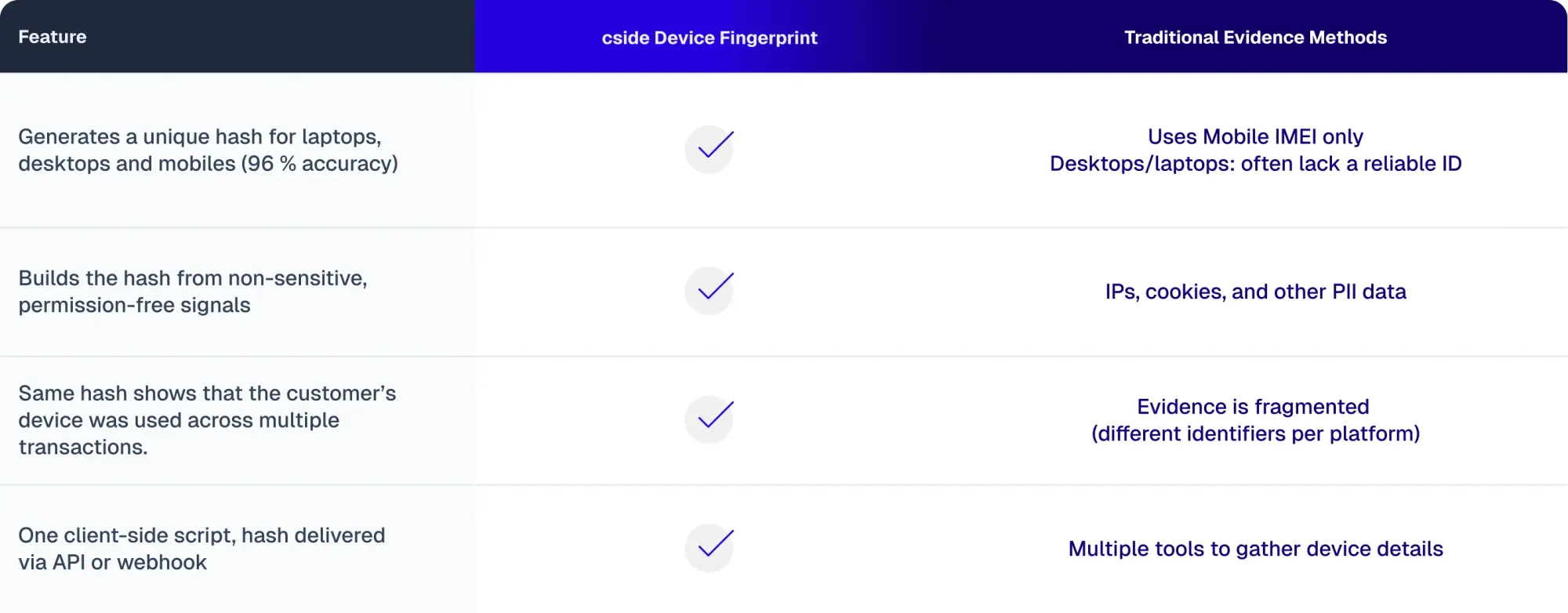

Device Fingerprinting v.s. IP Addresses and Device ID’s:

- **IP Addresses:**An IP can change any time you switch networks or locations. With VPNs and privacy browsers now common, relying on IPs for dispute evidence just doesn’t hold up.

- Device IDs: Basic device IDs (like IMEI on mobile) don’t exist across all devices and are easy to reset or spoof.

What is a device fingerprint?

- Device Fingerprint: In the context of VAMP (and online payment processing), a device fingerprint is a unique identifier created by combining dozens of software and hardware signals from a browser or device. A fingerprint produces a consistent “hash” that can reliably link transactions across sessions or accounts.

Is cside’s Device Fingerprinting privacy compliant?

- Yes, cside’s fingerprinting technology uses non-sensitive signals like screen resolution, time zone, and language settings to generate a unique hash.

Fingerprinting is actually less invasive than cookies or tracking pixels as it doesn’t store personal data or rely on consent banners. When implemented correctly this approach is privacy-friendly and compliant with frameworks like GDPR.

Comparison Table: Device Fingerprinting v.s. Traditional Evidence Methods

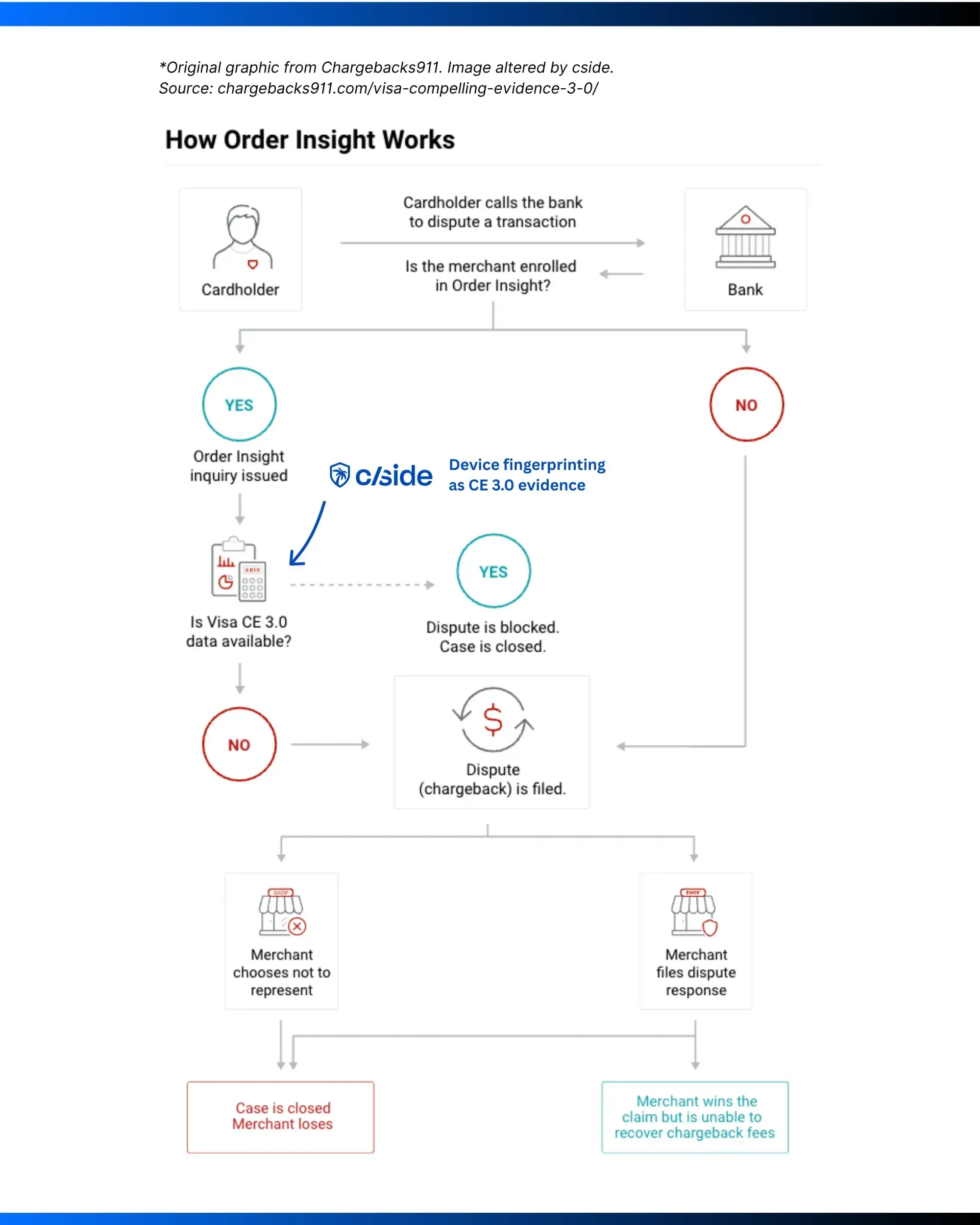

How Device Fingerprinting Reduces TC15s & Chargebacks

CE 3.0 success comes down to data quality. Merchants who feed Visa strong recurring identifiers win more disputes. And each of those CE 3.0 wins in your tracking column means less official chargebacks.

Infographic: How Device Fingerprinting Blocks Chargebacks

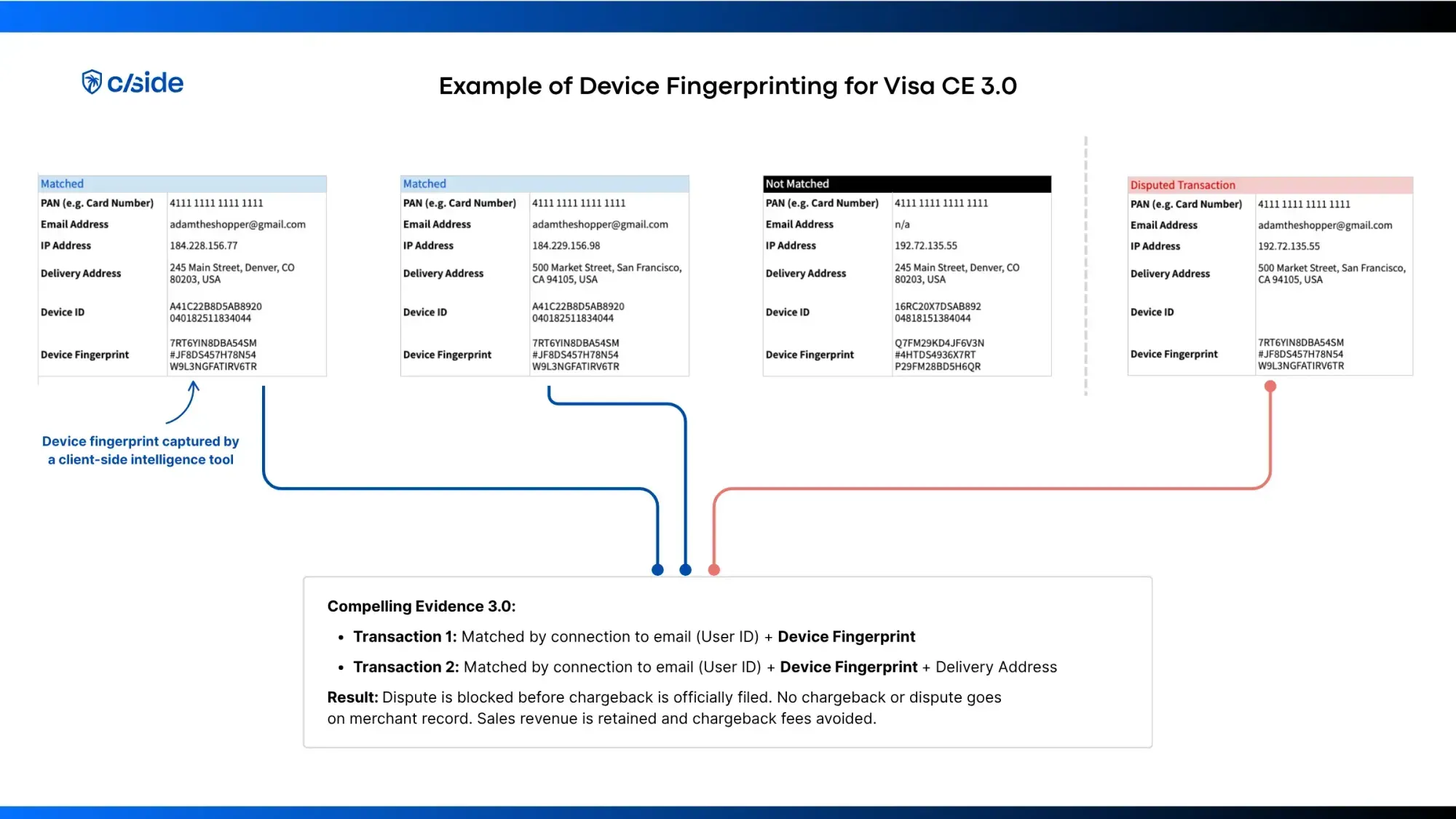

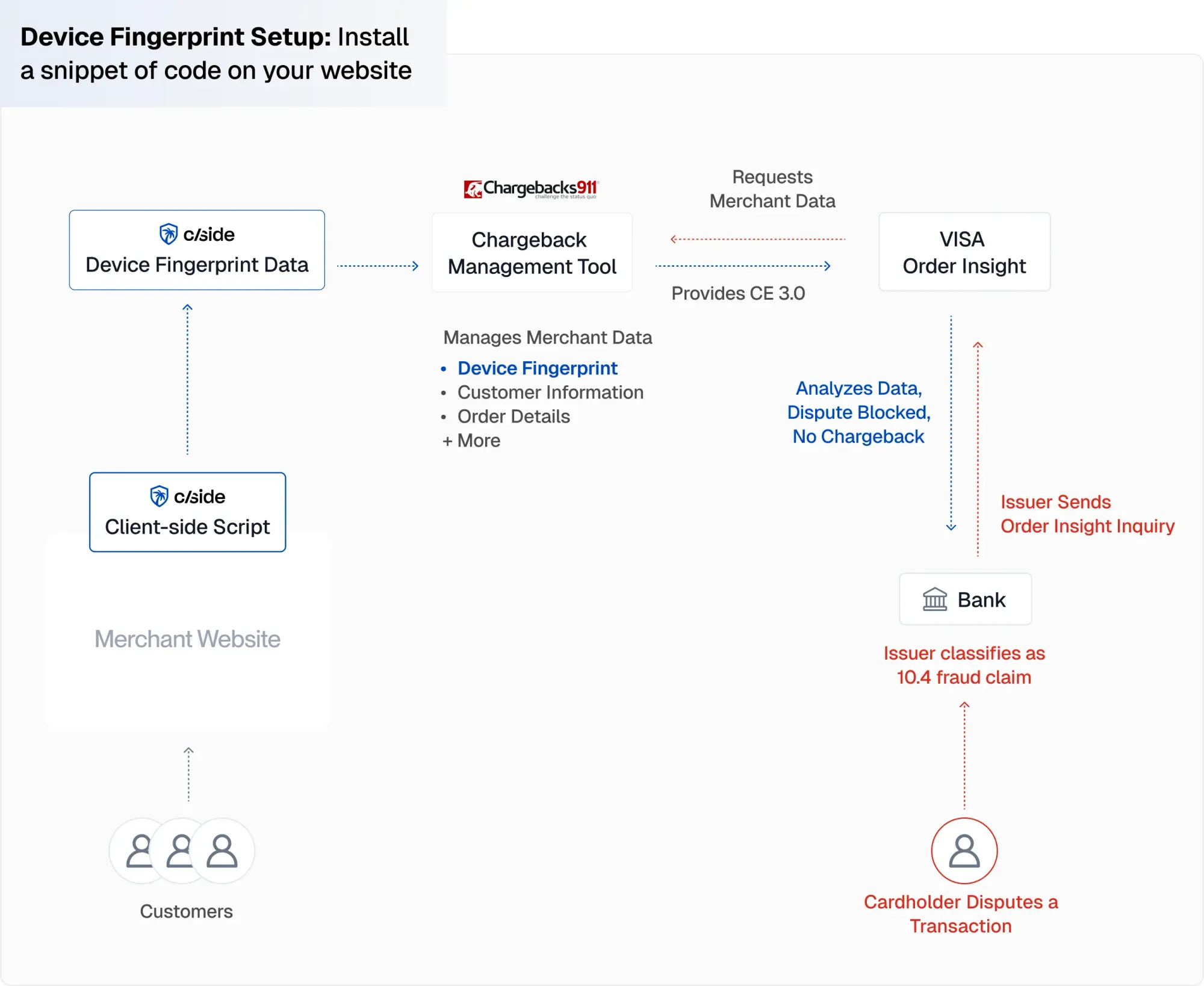

These evidence points prove to Visa that the transaction wasn’t truly a 10.4 card not present fraud case. It was a legitimate customer using the same trusted device as before. Order Insight confirms the match, flags the purchase as legitimate, and the case is deflected before it ever becomes a chargeback.

With Visa’s Order Insight working through your chargeback management tool, the match happens in seconds and liability moves off your plate instantly.

Your VAMP ratio & revenue are protected because:

- No official chargeback = no TC15 logged

- No official chargeback = no refund required

- Dispute rejected = TC40 removed

Example of Device Fingerprinting Match for Compelling Evidence:

Note: Matched transactions must be undisputed and within the 120 day / 365 day time window mentioned above.

What Types of Chargebacks Does Compelling Evidence 3.0 Block?

A payment risk analyst recently asked us “will blocking chargebacks prevent victims from getting their money back?”. This is a common misunderstanding as there are so many types of chargebacks and fraud types that get lumped together. Genuine victims of credit card fraud (such as identity theft) would not be affected through the Compelling Evidence 3.0 program.

Compelling Evidence 3.0 and device fingerprinting (in this context of chargebacks) relate to preventing first-party chargeback fraud.

- First-party chargeback fraud(also known as first-party misuse or friendly fraud): When a cardholder intentionally files a false chargeback to recover funds. In other words, the customer themselves initiates the fraud, not an external attacker. This typically happens when a buyer forgets about a purchase, regrets it, or has a scheme to abuse chargebacks for personal profit.

Some common examples of first-party fraud relevant to CE 3.0:

- **Refund Fraud:**The cardholder makes a legitimate purchase but plans to exploit the refund or return process. Sometimes this looks like “wardrobing” - buying an item, using it temporarily, and then sending it back for a full refund.

- Cyber Shoplifting: A customer makes a legitimate online purchase, then turns around and files a false chargeback to get their money back. It’s intentional theft disguised as a refund request. In some cases customers plan to resell high-ticket items for a profit.

- Friendly Fraud: The cardholder files a chargeback for a legitimate transaction. This category is termed “friendly” as it is often accidental. The customer may have forgotten about the purchase or a family member used the same card and device to place the order.

How to Add Device Fingerprinting to Your Chargeback Defense Stack

Fortunately, adding device fingerprinting to your defense stack is a straightforward project. You can plug in device fingerprinting to your existing chargeback infrastructure based on the solutions you are already using. Below are common approaches along with expected data quality and setup complexity:

Integrating Device Fingerprinting into Chargeback Management Tools:

Comparing Methods to Use Fingerprinting for Compelling Evidence 3.0

A) Chargeback management tool with a prebuilt integration

Some chargeback management platforms (like Chargebacks911) offer a pre-built integration to a client-side intelligence platform such as cside.

In this setup, cside executes the device fingerprinting on the merchant’s website. Data is synced Chargebacks911, which then enriches it with other merchant data such as order details, payment metadata, and account identifiers.

Chargebacks911 stores and delivers information to Visa’s Order Insight exactly the way they expect it. No scripts to maintain on your end. No engineers on standby.

Pros:

- **Automated setup:**Install a script on your website and start fingerprinting instantly. Native integration with Chargebacks911 means no APIs or manual data schema mapping, just faster dispute deflection from day one.

- Data usability: Combine cside’s specialized browser-level visibility with Chargebacks911’s dispute infrastructure for effective prevention.

- Full client-side protection: Access other protection features that network-level fraud tools miss such as enumeration attack blocking, eskimming detection, and AI bot identification.

B) Integrate device fingerprinting into your chargeback stack manually

Alternatively, you can integrate a standalone fingerprinting solution into your chargeback management system using APIs. This approach gives you full control but is engineering heavy and requires constant updates to align with VISAs program changes (which have been frequent lately).

Pros:

- Control: Full customization of data flow and architecture

C) Chargeback management tool with built-in fingerprinting

A few chargeback tools come with fingerprinting baked in. Rather than integrating with a specialized vendor they use a fingerprinting technology built in-house. Since these are often a side feature and not a core product the coverage and signal depth may be less precise.

And merchants miss the bigger client-side picture. Card testing bots, e-skimming scripts, and sensitive data exposures go unnoticed leaving the site wide open to other forms of cyber fraud.

Pros:

- Single vendor: Fingerprinting is included in the subscription tier. No add-on or integrations required.

The Business Impact of Compelling Evidence 3.0

Every blocked dispute is money saved. According to CNBC, businesses lose $100B+ per year to “friendly-fraud”. In addition to painful processing fees your business loses inventory and time. Fingerprinting evidence makes it easier to retain the sales revenue that you’ve earned. The outcome is simple: better data, more fraud deflected. Every extra device match could be a CE 3.0 win in your tracking column.

With the right data, you can achieve more “blocked disputes”. At this stage your VAMP ratios (TC15 + TC40s) are not impacted as the cases are considered to be closed early.

What This Means for Your Bottom Line

Reduce operational costs: Avoid chargeback fees (around $20/dispute), technical penalties (up to $250), and appeal costs.

<div class="card">

<div class="icon" aria-hidden="true">

<svg viewBox="0 0 24 24" fill="none">

<path d="M12 3l7 3v5c0 5-3.1 9-7 10-3.9-1-7-5-7-10V6l7-3z" stroke="#fff" stroke-width="2" />

<path d="M9 12l2 2 4-4" stroke="#fff" stroke-width="2" stroke-linecap="round" stroke-linejoin="round" />

</svg>

</div>

<p class="text"><strong>Protect your VAMP Ratios (TC15s):</strong> With CE 3.0, disputed friendly fraud transactions that are resolved early don’t count as TC15s in Visa’s VAMP ratio.</p>

</div>

<div class="card">

<div class="icon" aria-hidden="true">

<svg viewBox="0 0 24 24" fill="none">

<path d="M12 3l7 3v5c0 5-3.1 9-7 10-3.9-1-7-5-7-10V6l7-3z" stroke="#fff" stroke-width="2" />

<path d="M9 12l2 2 4-4" stroke="#fff" stroke-width="2" stroke-linecap="round" stroke-linejoin="round" />

</svg>

</div>

<p class="text"><strong>Lower risk of restrictions:</strong> Staying below a VAMP ratio of 0.5% prevents account restrictions or termination.</p>

</div>

<div class="card">

<div class="icon" aria-hidden="true">

<svg viewBox="0 0 24 24" fill="none">

<path d="M12 3l7 3v5c0 5-3.1 9-7 10-3.9-1-7-5-7-10V6l7-3z" stroke="#fff" stroke-width="2" />

<path d="M9 12l2 2 4-4" stroke="#fff" stroke-width="2" stroke-linecap="round" stroke-linejoin="round" />

</svg>

</div>

<p class="text"><strong>Recover lost revenue:</strong> Merchant revenue vanishes to “that wasn’t me” claims. Win back sales to stop the profit leak.</p>

</div>