TL;DR: chargeback indemnification versus pre-dispute blocking

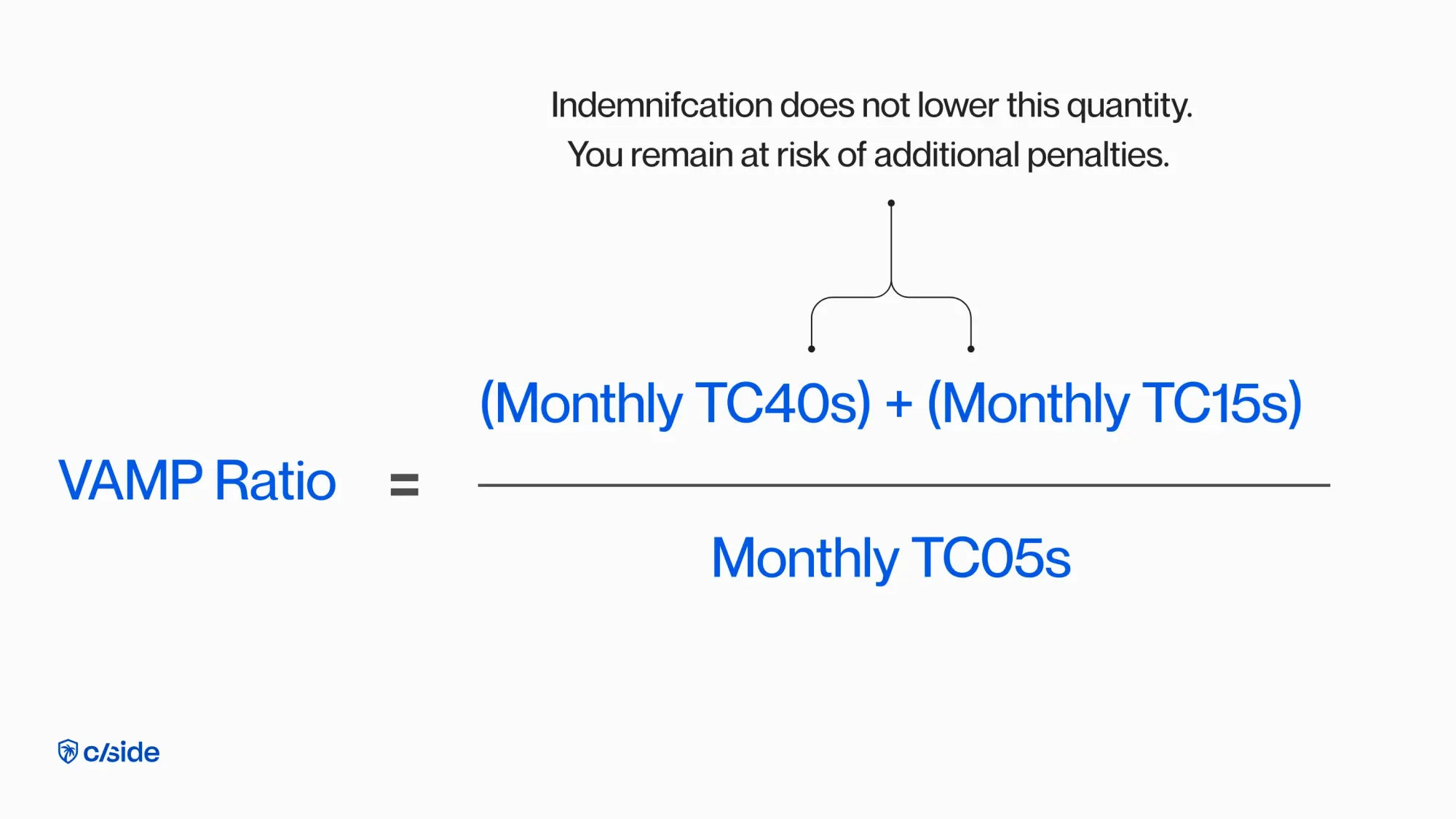

- Indemnification refunds your money, but it does not remove the TC40 or TC15 from the VAMP numerator. You can be fully indemnified and still breach the 1.5% Excessive threshold with $8-per-transaction fines that no insurance covers.

- cside's chargeback evidence solution cancels initial dispute requests before they generate TC40s, hitting both components of the VAMP ratio (fraud reports and chargebacks) rather than just refunding after the fact.

- If you don't know your current VAMP ratio and your dispute volume is growing faster than your transaction volume, indemnification is a cashflow patch on a risk-exposure problem. Switch layers before the acquirer offboards you to protect their own portfolio.

In This Blog:

- What Changed From VDMP/VFMP to VAMP (2025)

- Why Indemnification Doesn’t Protect Your VAMP Ratios

- Methods To Lower Your VAMP Ratio

- Penalties for High VAMP Ratios

For years providers of fraud and dispute management software used the statement “we’ll indemnify your successful chargebacks” as a safety net for their customers. If a dispute slipped through, the provider would reimburse you. And that is a good approach to protect your cashflow, however not your risk exposure. With today's VAMP ratio thresholds focusing on risk, those indemnification strategies don't protect the merchant anymore.

“A lot of indemnification strategies don’t work anymore with the new numbers. VISA’s requirement is 0.9% for merchants. The acquirers have to stay below 0.5% so many of the acquirers are adding another compliance level requiring merchants to be below 0.5%”

- Zak Matthews, Solutions Engineer, Chargebacks911

What Changed: From VDMP/VFMP to VAMP

Previous to VAMP, the TC40 didn't live in your ratio. Alerts haven't changed, the way the ratio is calculated has.

VAMP (Visa Acquirer Monitoring Program) tracks the rate of fraud and disputes against your processed volume. It penalises both the acquirer and the merchant for failing to meet certain thresholds related to disputed transactions. It replaces Visa’s former monitoring programs VDMP/VFMP and combines them into one rate that monitors fraud and chargebacks for acquirers and merchants.

TC40sare issued when the cardholder notifies their bank of a ‘not me’ transaction, right or not.

TC15sare are all the successful chargebacks, both fraud and non-fraud related ones .

TC05s are all the monthly settled transactions.

Two crucial observations:

-

It's volume based and not $$ based. A $10 dispute counts the same as a $10.000 dispute

-

It counts the disputes whether or not a provider indemnifies you. Meaning it will increase your VAMP ratio regardless.

Merchants are expected to stay ≤ 0.9% and many acquirers impose even tighter internal limits because they must stay below the ≤ 0.5% as a network. This means that a merchant at 0.8% may still be in violation of their acquirers policy, even if they are technically under the VAMP ratio threshold of ≤ 0.9%.

Lets do a sample VAMP calculation

Say you process 1,000,000 transactions per month and you incur 2,800 TC40s and 3,500 TC15s. Your VAMP ratio will be (2800+3500)/1,000,000= 0.63% meaning you’re still above the acquirer threshold of ≤ 0.5% (at risk of penalties) regardless if you use an indemnification strategy.

Why Indemnification Doesn’t Protect Your VAMP Ratios

- Indemnification fixes losses, not ratios: getting reimbursed for a chargeback does not remove the TC40s and TC15s from the numerator which increases your VAMP ratio and triggers fines, monitoring programs and potential termination

- It incentivises the wrong behavior: Some vendors only pay when a dispute becomes an official chargeback. This means merchants will let alerts turn into chargebacks so they can claim indemnity, but in the meantime blow up their TC40s and TC15s.

- The network is indifferent to who pays the bill: VAMP and issuer fraud reports count signals (alerts), not settlements. Whether your provider, your acquirer or you pay the fees is irrelevant to the network's view of your risk profile.

- Acquirers will pressure you: The acquirer must keep their ratio under the VAMP threshold of ≤ 0.5%. If your VAMP ratio is 0.7% (which is below the 0.9% threshold for merchants) you become a portfolio risk. That could trigger additional compliance, reserves, volume throttling or even offboarding.

- Trying to increase acceptance rates by using indemnification strategies: Lowering your fraud thresholds for transactions because they are indemnified anyway can be dangerous especially when the team managing acceptance rates may not understand the VAMP regulations and setting your organisation up for significant fines.

So How Do You Lower Your VAMP Ratio?

To manage your VAMP ratio you have to reduce the numerator of TC40s and TC15s. This means shifting your investments from reimbursement to pre-dispute blockingsolutions like the one of cside and Chargebacks911.

1) Lower your TC15swith RDR (Rapid Dispute Resolution) and CDRN (Chargeback Dispute Resolution Network). This prevents a dispute from progressing to a full chargeback and potentially becoming a TC15 (dispute code), but they do not prevent the issuance of a TC40 (fraud report).

2) Lower your TC40swith cside chargeback evidence solution for pre-dispute blocking and and cancel out the initial dispute request.

A High VAMP Ratio Hurts Your Business

If you breach your VAMP ratio, it's 6-8 dollars per TC15, if you’re over 0.7% it will be even higher and VISA keeps changing the fees. Moreover, that 6-8 dollars is not covered by any indemnification or insurance. Indemnification will always be more expensive than representation and if you’re worried about your VAMP ratio or don’t know it, it's time to make the business case.

Prevention Beats Reimbursement

Net-net: indemnification solved the pre-VAMP era problem of getting your money back. VAMP is today's pain for acquirers and merchants. Staying below the ratios will determine if you can keep processing at all. To achieve that you need a proven pre-dispute blocking solution.