TL;DR

- There are different stages of the ATO attack chain: credential acquisition, credential validation, account access, and account monetization. Different tools address separate steps in this chain.

- Mid-market or small business teams that want focused ATO protection will typically use a fingerprinting tool (like cside) that feeds signals into an MFA enforcement mechanism.

- Large enterprises with a fraud team looking to defend against multiple payment fraud vectors will usually use an anti-fraud suite like Forter or Sift.

- MFA alone is no longer enough to prevent ATO reliably. Session hijacking increased by 127% in 2025 (which bypasses MFA). Fingerprinting can still catch these compromised sessions through device and browser-level data.

How we evaluated these tools

An "account takeover" refers to a singular outcome: unauthorized access to an account with fraudulent intentions. But this fraud vector is not one-dimensional. Account takeover has multiple entry points, different signals, and different solutions that address separate layers of the attack chain.

This comparison separates tools by what they do. We wrote this guide to help fraud and executive teams understand the best combination for their risk profile when they are trying to reduce fraudulent chargebacks and protect their users from the $15.6 billion of losses due to ATO.

Different types of ATO prevention solutions

| Category | What it does | ATO stages covered | Example vendors |

|---|---|---|---|

| Full anti-fraud suites | Transaction scoring, post-login monitoring, cross-merchant ML | Account access, monetization | Sift, Forter |

| Fingerprinting solutions | Device and browser signal collection, identity matching | Credential validation, account access | cside, Castle |

| MFA solutions | Second-factor authentication at login | Account access | Okta, Microsoft Entra ID |

| WAFs / bot management | Network-layer protection, rate limiting | Credential validation | Cloudflare, AWS WAF |

Full anti-fraud suites

Full anti-fraud suites aim to be all-in-one platforms. They typically cover a range of fraud vectors including AML compliance, KYC verification, and payment fraud. These suites are powerful but expensive and rigid. Users report enormous enterprise price tags and configurations with false positives.

Platforms like Sift and Forter:

- Analyze transaction data like purchase amounts, payment methods, and shipping address changes to flag fraud patterns.

- Monitor post-login behavior for anomalies.

- Use machine learning for predictive risk scoring across all of these signals, training models on cross-merchant fraud data.

Full anti-fraud suites typically have some form of fingerprinting and device intelligence baked into their risk scores.

Fingerprinting solutions

Fingerprinting solutions collect device and browser-level data. When fingerprinting data on a new login mismatches the baseline, along with other signals, this is a strong indicator that an account takeover has occurred.

Platforms like cside:

- Detect signals of ATO including new devices, impossible travel, malicious VPN/proxy usage, and fingerprint mismatches.

- Catch bot and AI agent abuse such as credential stuffing.

- Feed signals into enforcement mechanisms like step-up MFA challenges or risk scoring to give anti-fraud systems the device intelligence they need to make better decisions.

MFA solutions

MFA solutions add a second verification step to the login process itself (think SMS or email verification). They don't detect fraud or analyze device data on their own. They make it harder to authenticate with stolen credentials in the first place.

Platforms like Okta and Microsoft Entra ID:

- Require a second factor like a push notification or biometric check before granting access.

- Can be used as a "step up" verification when a user logs in from a new location or unrecognized device.

Traditional MFA (SMS, email) is being increasingly bypassed by new attack playbooks. An analysis across 4.2 billion authentication attacks saw an increase of 127% in session hijacking instances in 2025.

Adjacent solutions

These are not dedicated ATO solutions, but they are often already deployed in organizations and serve a purpose in the ATO attack chain alongside other fraud vectors.

- WAFs: WAFs like Cloudflare and AWS WAF protect against broad web attacks like SQL injection and XSS, and most include basic rate limiting on login endpoints. They operate at the network layer and don't analyze device or behavioral signals, so they'll catch simple brute force attempts but miss credential stuffing spread across thousands of IPs.

- Bot management: These platforms separate human traffic from automated traffic using challenges, behavioral analysis, and IP reputation. They stop high-volume credential stuffing but struggle with AI-powered bots that mimic human behavior.

- Upstream credential intelligence: These services monitor dark web markets and infostealer logs for stolen credentials belonging to your users. They're purely preventive.

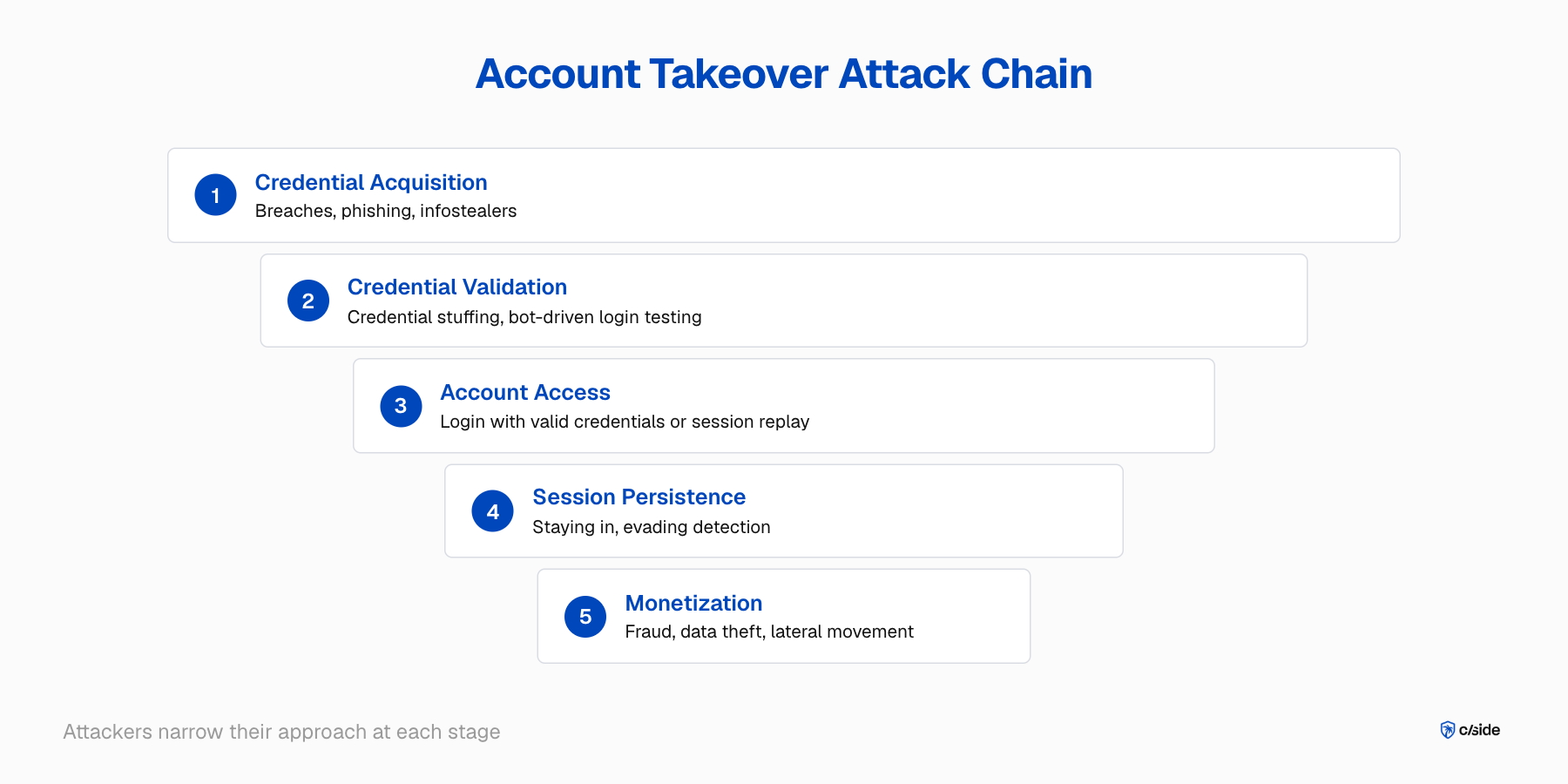

Mapping solutions to the ATO attack chain

Credential acquisition (breaches, phishing, infostealers) → Credential validation (credential stuffing, bot-driven login testing) → Account access (login with valid creds or session replay) → Session persistence (staying in, evading detection) → Monetization (fraud, data theft, lateral movement)

If you're just starting to look into ATO prevention, you don't need to cover every single stage. The illustration helps you understand where each tool sits. Different industries and risk profiles will care more about certain aspects of this attack chain. For example, the crypto industry (the most valuable ATO target in the U.S.) is subject to SIM swapping campaigns. Travel websites on the other hand are frequently targeted by session hijacking attacks where attackers steal cookies to get into loyalty accounts.

Related: takeover targets accounts that already exist. The upstream surface is fake new accounts, where attackers register at scale for trial abuse and multi-accounting. cside Signup Shield turns each registration into a real-time trust verdict to stop those accounts at signup.

Selection tips based on your risk profile

Large e-commerce company with a dedicated fraud team:

You're processing thousands of transactions a day and your fraud analysts are drowning in manual reviews across payment fraud and account takeover simultaneously. You want one platform scoring every event across the funnel.

Commonly used defense stack: A suite like Sift or Forter consolidates risk scoring, investigation dashboards, and chargeback workflows into one vendor. They deploy basic fingerprinting as part of their platform. This comes with an enterprise price tag, but if your fraud volume is high enough it may be worth the investment.

SaaS platform looking for flexible ATO signals:

Your core threat is account takeover and automated abuse on your platform. You need to know when a login doesn't look right, and you want to control what happens next inside your own product logic.

Commonly used defense stack: cside fingerprinting signals feed into your enforcement mechanisms. A device mismatch triggers step-up MFA through Okta. An AI agent detection fires a webhook to your SIEM. You define the rules and enforcement actions.

4 account takeover prevention tools to evaluate

cside

cside is a web security platform with a dedicated Fingerprinting product that helps identify account takeover attacks. Browser-layer signals give you real-time visibility into account takeover signals so you can block fraudulent sessions before they cause damage.

cside also offers a client-side protection solution that monitors your website for signs of session hijacking or phishing attacks injected through third and first-party scripts.

ATO prevention categories: Fingerprinting, Bot Detection.

Key features:

- Fingerprinting: Collects the full spectrum of device and network signals (IP, geolocation, VPN/proxy detection, browser version, OS, screen resolution) to build a unique identifier for every visitor that touches your site.

- ATO signals: Combinations of signals (impossible travel, unknown device, one device accessing multiple accounts) to highlight suspected ATO sessions.

- Inform enforcement actions: Fingerprinting signals feed directly into your enforcement logic. Flag a session for step-up MFA, block it outright, or log it for review based on risk score thresholds you define.

- Website monitoring: Monitors your site's client-side environment for malicious scripts that attempt to steal credentials or redirect users to phishing pages.

- Specialized AI agent detection: Detects fraudulent AI agents that evade traditional bot detection (like CAPTCHAs or rate limiting) to carry out credential stuffing attacks.

Helps with these stages in the ATO attack chain:

- Account access: Detects when an account is accessed from an untrusted device or location.

- Credential validation: Catches credential stuffing and other forms of bot abuse by identifying automated tools at the browser level.

Best for:

- Teams that want flexibility: cside gives you access to raw fingerprinting signals and pre-built risk score templates, but lets you customize thresholds and rules to fit your own anti-fraud workflows rather than locking you into a black-box score.

- Developer-led teams that want raw data: The API and webhook means you get device intelligence as structured data you can pipe into your own scoring engine or custom detection logic.

Reviews:

- 4.9/5 on SourceForge (37 reviews and ratings shown: 25 native SourceForge reviews plus 12 verified third-party ratings surfaced there).

- 4.8/5 on G2.

Pricing:

- Free tier and free trial.

- Business plan starts at $99/month.

- Enterprise pricing requires custom quote.

Castle

Castle is an account security and fraud prevention platform that combines device fingerprinting, real-time risk scoring, and a no-code policy engine. It returns three scores per event (Bot, ATO, and Abuse) and supports both web and mobile through native SDKs.

ATO prevention categories: Fingerprinting.

Key features:

- Device fingerprinting with risk scores: Collects device, network, and behavioral signals and returns real-time Bot, ATO, and Abuse scores (0-100) per event so you can set enforcement thresholds without writing custom scoring logic.

- No-code policy engine: Build and update fraud rules without deploying code. Set conditions based on risk scores, device attributes, or velocity patterns and trigger actions like allow, challenge, or deny.

- Mobile SDKs: Native support for iOS, Android, React Native, and Flutter with mobile-specific signals like jailbreak detection, emulator detection, and rooted device detection.

Helps with these stages in the ATO attack chain:

- Account access: Scores every login event against device and behavioral baselines. Flags new devices, location anomalies, and risk score spikes for challenge or deny actions.

- Credential validation: General bot scoring detects automated login attempts, though it does not differentiate AI agents from traditional bots.

Best for:

- Teams that need web and mobile app coverage. Castle ships native mobile SDKs with signals like jailbreak and emulator detection that web-only platforms don't offer.

Reviews:

- 3.7/5 on G2.

Pricing:

- Free plan available.

- Starter plan begins at $200/month.

- Enterprise: custom pricing.

Okta

Okta is an identity and access management platform that adds multi-factor authentication and adaptive risk-based login policies. It strengthens the authentication layer by requiring additional information beyond a username and password combination.

ATO prevention categories: MFA.

Key features:

- Adaptive MFA: Evaluates login context like device, IP, geolocation, and velocity to decide whether to prompt for an additional factor. Legitimate users on recognized devices pass through with minimal friction, while anomalous logins trigger step-up challenges.

- Passkey and FIDO2 support: Supports passwordless authentication via WebAuthn, allowing users to authenticate with device biometrics instead of passwords, eliminating credential stuffing as a vector entirely.

Helps with these stages in the ATO attack chain:

- Account access: Blocks attackers who have valid credentials but can't pass the second factor. Adaptive policies catch anomalous login context that static MFA would miss.

Best for:

- Organizations that need identity infrastructure, not just ATO tooling. Okta is an identity platform first. It consolidates SSO and lifecycle management alongside MFA.

Reviews:

- 4.5/5 on G2.

Pricing:

- Starter Suite: $6/user/month (includes MFA).

- $1,500 annual contract minimum.

Sift

Sift is a full anti-fraud suite that covers account takeover as one module alongside payment fraud, content abuse, and chargeback management.

ATO prevention categories: Full anti-fraud suite.

Key features:

- Real-time risk scoring across the user journey: Scores signups, logins, transactions, and account changes using ML models trained on cross-merchant fraud data.

- ActivityIQ (generative AI): Summarizes risk patterns across multiple accounts and sessions using generative AI.

- Global identity network: Links device, behavioral, and identity signals across Sift's merchant network. A device or identity flagged for fraud at one customer raises risk scores across the platform.

Helps with these stages in the ATO attack chain:

- Account access: Scores login events against behavioral baselines and cross-merchant intelligence to flag compromised accounts.

- Monetization: Monitors post-login behavior like transaction velocity spikes, shipping address changes, and payment method additions to catch attackers.

Best for:

- Enterprise teams with a fraud ops team and dedicated budget to reduce fraud. Sift consolidates ATO, payment fraud, content abuse, and chargeback management into one platform.

Reviews:

- 4.6/5 on G2.

Pricing:

- No public pricing. Sift requires a custom quote and typically targets enterprise contracts.

What's changing in 2026

The cost of ATO is climbing. ATO-related chargebacks cost merchants $576 per incident (76% higher than a regular chargeback according to Equifax). Chargebacks are extremely common after a successful account takeover as attackers make fraudulent purchases. Merchants have very little defense in these cases as it was genuine fraud. The only real prevention mechanism is to prevent these cases from occurring in the first place.

MFA was a strong defense mechanism for a while (and still a foundational layer) but sophisticated attacks now frequently bypass this defense altogether. A well-known example was the Crypto.com account takeover breach that lost $30M+ of customer funds from an attack that bypassed 2FA. There are a couple of rising hacker toolkits that are enabling the evasion of MFA.

A type of attack we have seen at cside is where attackers inject a CSS overlay on a legitimate site that redirects users to a fake login page. The user doesn't notice anything wrong because it looks identical to the real one. An Adversary-in-the-Middle (AiTM) proxy sits between the user and the real login page. The user logs in normally and enters their MFA code, then is even redirected back to a legitimate page. But the attacker's proxy captures the session token that gets created after authentication and uses it to walk right into the account.

This is only one client-side attack type. cside research shows that tens of thousands of websites are affected by client-side attacks in 2025. These sophisticated attacks target high-value accounts such as travel accounts (loyalty points), crypto accounts, or enterprise finance apps.

Reduce account takeover attacks with cside

cside gives you device intelligence and browser-level signals to detect compromised sessions before they cause damage. Start with a free plan or book a demo to see how fingerprinting fits into your ATO prevention stack.